April 2023: Show Me the Money

![]()

Show Me the Money

April 11, 2023

Dow: 33,684

The depositors in many regional banks seemed to echo Cuba Gooding Jr’s famous line from the movie Jerry Maguire, “Show me the money.” The bankers’ response seemed to echo Jimmy Stewart’s from It’s a Wonderful Life, “The money’s not here, it’s in Joe’s house” and other income producing investments. A great example of how a bank is a collection of assets and liabilities, loans, and deposits. That little thing called leverage also usually plays a role in fast moving liquidity crises. No bank can sustain a short-term demand for the return of a majority of its deposits – a bank run. It is the job of the banks individually, and the government and regulators as a whole, to ensure that there is confidence in the system. The failure lies both with the management of the banks, and with the regulators and government officials tasked with both limiting the risk that there will be a bank run and reacting appropriately to stop it when it happens.

The stock market is up since its recent low of March 13, which was higher than its December low, which was higher than its October low. So far, markets and the economy are holding up in the battle against the Fed’s effort to slow the economy and raise unemployment. The battle is not won. There are unforeseen fragilities in the system, as the struggles in the banking system demonstrated last month. First quarter earnings will provide a barometer of how the economy is holding up through the most recent rate increases. We expect that the news will be largely positive. Companies have discovered a new focus on controlling costs and focusing on profit. Consumers are largely optimistic as they have seen inflation roll over in the second half of 2022. The immediate shock of higher mortgage rates is working its way through the housing market. Supply chain issues have continued to abate, which helps businesses plan better and optimize their operations.

The Treasury market has shown significantly increased volatility as banks became more stressed. Even as the Fed raised rates at their March meeting by 25 basis points, Treasury yields fell across the yield curve. The two-year Treasury fell 80 basis points in March, and the ten-year Treasury fell 45 basis points. Instead of expecting Fed Funds above 5% by year end, the market now expects rates to be cut at least three times by year end.

There have been three Fed rate hiking cycles since the late 1990’s, and we are now in the fourth. In every case where the two-year Treasury yield dropped below the Fed Funds rate, the next Fed rate move has been a cut. The two-year Treasury dropped below the Fed Funds rate in June of 2000, and the Fed cut rates six months later. It happened again in July of 2006, and the Fed did not cut rates until 15 months later. The Great Financial Crisis followed, and the S&P 500 Index did not bottom until eighteen months after the first rate cut. In the third instance, the two-year Treasury dropped below Fed Funds in March of 2019, and the Fed cut rates four months later. The ten-year Treasury yield moving below the three-month Bill yield may be an even better indicator of imminent Fed rate cuts, and that spread has been negative for five months.

Some indicators of economic activity are slowing without an abrupt reversal, and the labor market seems to be softening ever so slightly. These are both excellent signs because they demonstrate that the economy may remain healthy as we approach the end of the Fed tightening cycle – the proverbial ”soft landing.” Corporate earnings and company outlooks will be insightful as they begin to be reported for the first quarter.

Market returns have been respectable in the first quarter in both the stock and bond markets, representing a partial recovery from 2022 returns and recognition that we may navigate this Fed tightening cycle without material damage to the economy. If we had to pick one economic indicator to use to navigate the markets, it would be the unemployment rate. As long as we do not see a material rise in unemployment, the economy should be able to navigate higher short-term rates without a slowdown.

There seems to be a significant amount of pessimism present among market participants, evidenced by declining long-term Treasury rates and expected Fed rate cuts in the back half of the year. Higher than normal pessimism is usually accompanied by market opportunities, and we seek to take advantage of these opportunities.

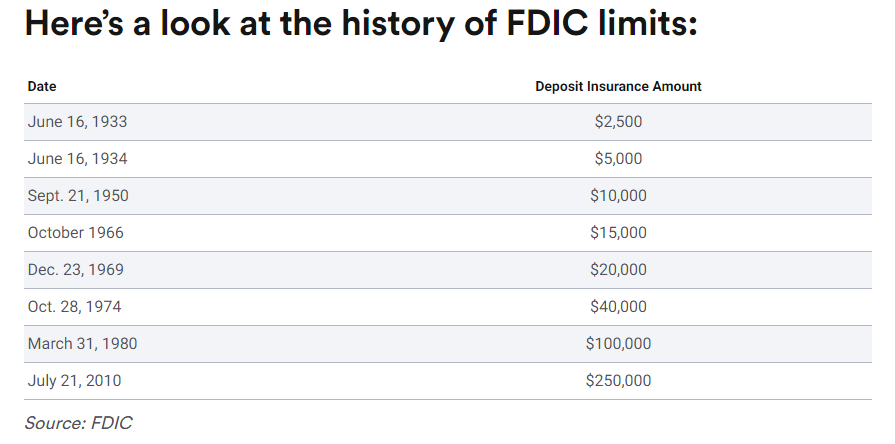

Random thought: FDIC Insurance historically had limits, until it recently seemingly didn’t: