![]()

Growth vs. Value

September 29, 2020

Dow: 27,452

Growth or value? This question has been a facet of investing for decades, but has come into even more pointed focus in the last few months. Growth stocks have continued a decade-long trend and massively outperformed value stocks for much of 2020, but in recent weeks, performance has been more even. The change suggests many of the factors that propelled growth forward since the pandemic have been fully absorbed by the market. But is that enough to stage a changing of the guard for value investing?

We believe two main factors benefited growth stocks coming out of the pandemic-induced economic slowdown. First, the areas of the economy that the pandemic hurt most tended to be lower-wage, lower-productivity industries that provide person-to-person service. Examples include retail, transportation, airlines, hotel, and restaurant industries. By and large, these are value stock categories. Energy stocks, which are another large component of value indices, were also punished as the economic slowdown dampened demand.

Companies in higher-productivity areas, such as technology, were less affected by the pandemic. These businesses primarily fall into the growth category. Expectations of an extended low inflation environment have also supported growth stocks. Growth stocks’ valuation is based largely on the stream of earnings they will earn in the future. Low inflation means the value of those future earnings streams are worth more because they won’t be inflated away.

These metrics had helped push growth stock valuations higher in recent months. At some point, markets were bound to reassess extreme valuations. That has happened recently with the tech-heavy NASDAQ falling 10% into correction territory just three days after setting an all-time high at the beginning of September.

Meanwhile, low inflation is a headwind for a value company. These companies generally have more leverage than growth companies. If there’s low inflation, a dollar in the future maintains its value. Lower inflation increases the debt burden of leveraged companies in real dollar terms. Low inflation also makes it more difficult for these companies to raise prices or increase revenue to aid in servicing their debt.

The recent slump by growth stocks has put growth and value performance roughly in line with each other since the end of July. Many wonder if extreme valuation differences between growth and value stocks mean value is now due for its own run of outperformance. For this to happen, we think the market will need more signs of economic improvement.

Value stocks are typically more economically sensitive than growth stocks, but that is even more true in the recent downturn. To a large extent, value stocks are associated with companies that primarily benefit when people are moving around and spending money. That just doesn’t happen when people are nervous about coming out of their homes and engaging in direct social contact with other individuals.

However, news about the virus has started to sound more encouraging. Although the number of new daily confirmed cases remains high, the infection rate is trending down as the number of confirmed cases divided by the number of tests is falling in many areas. Offices are starting to reopen. For example, JPMorgan recently announced it will call its traders back to their New York offices. Once we see more states reopen and the economy begin to rebound, we wouldn’t be surprised to see value outperform growth.

At Dana, our strategies are core equity strategies. We look for investments that have characteristics of both growth and value stocks. We are valuation-conscious, but we don’t make directional calls in our portfolio with an intentional shift toward value or growth. However, some of our strategies have started to take advantage of attractive valuations and invest in companies in the hotel, travel, and restaurant industries that would benefit as the economy gradually reopens.

We are also finding opportunity in stocks that have a good “self-help” story. The one silver lining in the recent downturn is that it has forced management teams to re-evaluate costs and think hard about how they can run their business more efficiently. Many have cut their capital expenditures or are looking for ways to deploy them more efficiently. We believe some of these businesses are poised to come out of the downturn running leaner than ever and could see a substantial earnings boost with even a modest economic lift. We will continue to perform our due diligence on these companies in the months ahead and deploy capital where we see opportunities develop.

Random thought: “Leave nothing for tomorrow which can be done today.” – Abraham Lincoln

![]()

New Normal

July 30, 2020

Dow: 26,314

“New normal” is a term that has been used to describe the economic circumstances that existed after the 2007-08 recession. Large amounts of personal wealth and capital were lost as housing values plummeted, stock prices fell, and jobs were lost. It took the stock market five years to recover, the housing market ten years, and the number of employed Americans seven years to reach their prior peaks. The term itself is oxymoronic: can something that is new be normal? We are dealing with much that is new this year – none of it seems normal.

We now have experienced four full months of the work from home economy. Surveys indicate that in early May, 70% of the workforce was working from home some or all of the time. By late July, roughly half of the country was still working from home some or all of the time. We would have doubted that such conditions could exist for this long without seriously impairing the long-term health of the economy. Huge amounts of fiscal stimulus dollars have offset the pain, but that flow of dollars is unlikely to continue at its current level, and Congress has not yet agreed on the form or delivery method for additional support. The S&P 500 is flat for the year and reached a new five-month high last week. The NASDAQ index is up 15% for the year. Does the performance of this year’s leaders in the market make sense? Google just became the fourth U.S. company to reach one trillion in market capitalization. Apple, Microsoft, and Amazon have now all rocketed to $1.5 trillion in market capitalization. In almost all past market environments where large companies have moved to high price to earnings ratios, they have gone through ten- to twenty-year periods where their stock performance has been flat. While we own and like these stocks, we will remain active and defensive within our allocation as we think its “Buyer Beware” for passive index investors getting historically high position concentrations.

We are at another key turning point in the battle against COVID-19. The confirmed caseload has increased significantly, mostly in southern states. Although the increased caseload has put pressure on the healthcare system, daily deaths are down from the levels of April and May. Still, daily deaths have moved up in the last week, and some areas of the country have imposed increased restrictions. School openings are the next challenge; some large districts will begin with remote learning. This will have economic implications as we can expect that family routines will be further disrupted during the coming school year.

COVID-19 appears to be the election issue that the Democrats have chosen to run on. With COVID-19, the new normal is always a moving target. If cases are increasing and fear and economic dislocation is worsening, it would seem to erode significantly the benefits of incumbency. If conditions are improving as we move towards the election, the incumbent politicians will try and play that factor to their advantage. Politics is like the markets in that the direction of change, or the perception of the direction of change, is usually more important than the current condition. There has been little that is normal in the Trump presidency, so why should this be a normal election? Biden has done a good job staying out of Trump’s way, but his potential weaknesses are readily apparent. Because of the cross currents of COVID-19 and societal upheaval, we find this election very difficult to handicap, even though we are less than four months out.

We are excited that our clients and consultants are finding new ways to combine some of our strategies to create robust portfolios for the current environment. Our Limited Volatility Strategy is low risk but still yields more than comparable investments. It can be combined with the Dana Preferred Stock Strategy, which yields over 5%, in a ratio that meets clients’ needs for income and security. Our newest equity strategy is the Unconstrained Equity Strategy, which focuses on disruptive companies with high growth prospects. As the Strategy has the freedom to hold a higher cash position in periods of market stress and currently holds concentrated positions in several disruptive technology companies, performance has been very compelling in the first six months of the year. Some investors have paired this strategy with an allocation to one or more of our other equity strategies to create a slightly more opportunistic equity portfolio.

These are dynamic times, and we are excited by the challenges we face. The investment landscape is far different than it was six months ago. Know that we are here to help you succeed in these times.

Random thought: “ He who is unfit to serve his fellow citizens wants to rule them.” – Ludwig von Mises

![]()

A Tour of the S&P 500

May 27, 2020

Dow: 25,548

Like most aspects of life since the outbreak of COVID-19, this Memorial Day weekend was unlike those in the past. The majority of us did not travel, swim or go to the beach, cook out with friends, or hug our parents or grandparents. Our entire investment team looks forward to a time that they can analyze business prospects and make investment decisions without considering the far-reaching effects of the virus on society. There is still much that we don’t know about the virus even as case levels plateau and decline in many areas of the country that were hit the hardest. We are moving into a phase where government directives will play a smaller role in the fight against the virus, and personal decisions and responsibility will play a larger role. As more people are free to interact and resume their normal schedule, will they do so, or will behaviors and economic decisions be altered for a long period of time? As we move into this next phase, just because we are free to do more, it does not mean we will. Nevertheless, we are creatures of habit; we just don’t know if most will resume their old habits or the new habits molded by COVID-19.

Since travel is limited, let’s take a virtual tour of the S&P 500 index. Many clients have asked us how the index can be down less than 9% this year through May 22nd when the total number of Americans receiving unemployment benefits has gone from two million to twenty five million in less than three months and the unemployment rate has reached 14.7% and could hit 20% in May. The S&P 500 is a capitalization weighted index; the largest companies by market capitalization, or total value of common stock outstanding, comprise the largest segment of the index. The five largest companies, Microsoft, Apple, Amazon, Google, and Facebook, make up about 20.6% of the index. The smallest 350 companies also make up 20.6% of the index. The largest companies have generally fared best during this crisis, and many smaller companies have fared worst.

If we look at the twenty-four industry groups that make up the index, it becomes easier to see how COVID-19 has affected some segments of the market far more than others. The three largest industry groups are software and services, media and entertainment, and pharmaceuticals and life sciences. These three groups comprise almost one-third of the index by market capitalization, and all three groups have positive performance for the year to date period. The fourth largest group is retailing. Most perceive retailing as one of the sectors that has suffered most since March, but the three largest companies in this group are Amazon, Home Depot, and Lowes, and all are up for the year. These companies and industry groups could be labeled the “haves.”

The energy group, which includes Exxon, Chevron, and ConocoPhillips, and represents less than 3% of the S&P 500 index, is one of the “have nots.” Real estate has also suffered, but that industry group also represents less than 3% of the index. The transportation group includes both trucking companies and airlines, but is less than 1.7% of the index. Hotels, restaurants, and cruise lines represent one of the hardest hit groups, but that group also makes up less than 1.7% of the index. These four groups contain most of the companies that were most harmed by the COVID-19 outbreak, but they represent less than 10% of the S&P 500 index.

Another way to understand the dichotomy of the haves and have nots is to compare the S&P 500 capitalization weighted index with the equal weighted index. Year to date, the commonly cited cap weighted index is down about 8%, while the equal weighted index is down almost 16%. Only about one-third of the individual stocks in the index are up more than the overall index. Over half of the companies in the index are down more than 16%, so if you chose stocks by throwing darts at a list of the companies in the index, you would most likely be disappointed with their performance this year. Another way to understand the performance differential due to size is to look at Ford and General Motors. They are perceived to be large companies when viewed in terms of their revenue or number of employees. Apple and Microsoft are each 23 times larger than Ford and General Motors combined when measured by market capitalization.

The fixed income markets have continued their measured recovery since the end of March. The yields on mortgages, municipal bonds, and corporates are as attractive as they have been in years when compared to Treasuries. It is likely that the Federal Reserve will keep rates low again for an extended period of time, but as markets stabilize, there is room for yields on many fixed income securities to fall and total returns in this area of the market should still be positive for the year and higher than the current yields. Over the last few weeks, even lower-rated companies have been able to issue new securities at higher yield levels, and these bonds have also typically increased in price in the secondary market. These bond issues have also helped to strengthen company balance sheets without the issuance of dilutive common equity shares.

The markets are said to be forward looking. We believe that is true, and we hope that the higher market levels of the last two months portend a successful recovery from the trauma and uncertainty of this spring.

We hope you all continue to stay safe and healthy.

Random thought: “How very little can be done under the spirit of fear” -Florence Nightingale

Supporting our Front Line Workers

Now more than ever, Dana believes it’s important to give back. This past month, we wanted to do something to assist those helping our most vulnerable through these uncertain times. Our employees raised funds and partnered with a local manufacturer to secure personal protection equipment for those on the front lines. We donated more than 1,300 shields to local hospitals, nursing homes, and law enforcement agencies defending against the coronavirus.

![]()

Strange Days Indeed

April 27, 2020

Dow: 24,134

We can’t help but continue to hear the lyrics of the Lennon song – Nobody Told Me – running through our heads. Virtually every day brings a new twist in the virus story. Some areas of the country are showing declines in growth rates of virus cases, some areas have yet to show any spike. We don’t know when the first cases appeared in the U.S. because we weren’t looking for them and we did not know how to identify mild cases and differentiate them from other flu strains. The lack of scale in timely testing has continued to hinder our understanding of the disease and its progression through the population. There are still unanswered questions about the communicability of the disease, morbidity, acquired immunity, period of infectiousness, and mutation. We also have no clear view of how the disease progresses within the body or what countermeasures are most effective. Even the efficacy of ventilators has been questioned.

This period of time has been unique even for investment managers, who are accustomed to making decisions under conditions of uncertainty. We are now entering a period where we hope the growth in identified cases will continue to decrease, even as economic activity and personal interactions increase as restrictions are eased. Can we slowly reopen closed businesses and institutions and expect a return to the status quo? Most certainly not. Some individuals will return to their prior routines, but many will change their behavior, some for a long time. How will this affect travel, business, consumption, investment? We have to try to decipher and anticipate new trends.

If the markets can be viewed as somewhat efficient and forward looking, maybe we can expect a return to a greater level of normalcy fairly quickly. The S&P 500 has recovered more than half of its decline from its February peak, and many growth indexes have recovered most of their declines for the year. Eight states never issued stay at home orders. A handful will relax restrictions in the last week of April, and more will relax recommended restrictions on activity in early May. The fiscal and monetary measures that were undertaken to address the Covid-19 problem were larger and implemented far more quickly than any in history. Even with relaxed restrictions, the elderly and those with health problems will still have to be extremely careful in how they interact and the precautions that they take. Our post-virus world will be different than our pre-virus world. Travel and hospitality industries will be significantly changed.

Our investment teams have been following the evolving virus situation in China since January and began making changes in the portfolios in early February. Exposure to leisure, hospitality, and travel industries was reduced or eliminated. Technology and consumer companies that bore a lower degree of negative exposure under the new stay at home economy were added. Healthcare companies that would play a role in addressing the virus were added, and more defensive, less cyclical companies were added in the industrial sector. Because these changes needed to be made to address the new reality, you will see a greater amount of trading in our equity portfolios than is typical. Strength of balance sheets became a top priority. Companies that can succeed regardless of the new uncertainties were added.

In the fixed income portfolios, the foresight to limit trading in a stressed environment helped us weather the storm. Far less trading was done, but prudent changes were made. The large reduction in Treasury and money market yields due to significant cuts by the Federal Reserve increased the relative yield advantage of the Limited Volatility strategy. In the middle of March, when fear and uncertainty were reaching their peak, many fixed income securities moved down 5% or more, and the typical market makers stepped away or made markets that drove the cost of liquidity up to hundreds of basis points. Like equity markets, most fixed income markets have recovered more than half of their declines and with rates likely to stay low, have room to generate continued total return gains as the economy heals.

As we move forward, a large degree of economic and financial uncertainty continues to exist. We have actively managed all of our portfolios in light of new information as it evolves, and we will continue to look for opportunities to improve the portfolios going forward as conditions change. We appreciate your patience through this stressful time. Feel free to reach out to us if we can help by sharing any information or insights, and continue to practice habits that will keep you and your families as safe as possible.

Random thought: Nothing happens quite by chance. It’s a question of accretion of information and experience. – Jonas Salk

![]()

Infodemic

March 2, 2020

Dow:

Fear is the virus on which the news media thrives.

Viruses are with us everywhere and always. Illnesses defined under the umbrella of influenza kill between 10,000 and 50,000 Americans each and every year. Total annual deaths in the U.S. are about 2.8 million, so influenza makes up less than 2% of those deaths. Video of personnel in gowns and masks carrying sprayers invoke the fear response.

Past influenza epidemics include the 1957-58 Asian flu, the 1968 Hong Kong flu, and the 2009 Swine flu. The H1N1 Swine flu appeared in the United States first. There were estimated to be 60 million U.S. cases, but only 12,000 deaths. Worldwide, the Swine flu is estimated to have killed 200,000-500,000 people – 80% of those deaths were people under the age of 65.

So, what do we know so far about the current Coronavirus? Like most flu strains, it preys on the elderly and the infirm. So far, death rates have been significantly higher for those over 65, with the death rate increasing with age. Respiratory disease and diabetes also significantly increase the mortality rate. This is unlike the 2009 Swine flu in a good way, which preyed upon the younger and most productive. Most flu strains end up infecting a significant portion of the population. It is likely there have already been far more unconfirmed than confirmed cases, which would mean the actual mortality rate is far lower than the current published rate. The mortality rate for those who are healthy and younger is also significantly lower than the average.

There are a number of current responses that will probably help reduce the transmission rate and the mortality rate for this epidemic, at least among the developed countries. Hygiene is the most important, and more people will take precautions and wash their hands. The main human behavioral response is to reduce gatherings. That is also taking place. The medical community will sequence the genome of the virus, and this will enable some sort of vaccine to be developed. Warmer weather in the northern hemisphere may slow transmission, although this is yet to be seen. When the virus is identified earlier, it will allow the medical community to more aggressively treat those who have been infected, probably again lowering the mortality rate.

Fixed income investors have been the beneficiaries of the pain in the equity markets, as rates have fallen significantly. Corporate spreads have widened as equities have fallen, but lower Treasury rates across the yield curve have provided a tailwind to all fixed income. If markets do not stabilize soon, expect the Fed to react either with further comments or actions. Recent market volatility highlights the value that owning bonds within balanced portfolios can provide to long-term growth and stability.

We have had a sharp market correction in the last week, with most equity market indices declining over -10%. Corrections can happen for many reasons, and they are not terribly uncommon, although they have been less common during the current economic expansion. Will this outbreak reduce economic activity? Yes, but probably only temporarily. All virus outbreaks are serious and result in a tragic loss of life, but this virus outbreak may be more deadly than those that we have had in the past – only time will tell. One significant positive this time around is that it does not seem to attack the healthiest in our society as some past epidemics have. The markets seemed to show some signs of stabilization into the close last Friday, and we will continue to monitor events closely and adjust portfolios accordingly.

Some relevant articles are linked below:

https://www.bbc.com/news/health-51674743

https://www.realclearscience.com/blog/2020/02/29/five_reasons_you_dont_need_to_panic_about_the_covid-19_coronavirus.html

https://www.bloomberg.com/opinion/articles/2020-02-29/coronavirus-end-game-will-be-nuisance-more-than-terror?srnd=premium&sref=ZaVmU2eP

https://www.bloomberg.com/opinion/articles/2020-02-29/coronavirus-prep-checklist-a-rational-guide-for-covid-19?srnd=premium&sref=ZaVmU2eP

Random thought: The earth’s solar year is 365.24219 days long. Adding a day every 4 years moves us slowly ahead of the solar calendar. To adjust, we leave off a leap day every 100 years, but add it back every 400. 2000 was a leap year, the next century leap year is 2400.

![]()

Smorgasbord

February 25, 2020

Dow: 27,081

We are going to try and briefly touch on a number of different topics in this viewpoint. All are important to the markets, but we have no closure on any of them. In such cases where strong conclusions cannot be drawn, brevity is probably a virtue.

First is the Coronavirus; as the disease progresses, the Chinese government has slowly exercised an increasing degree of control over the information flow. Early on, there were foreign news agencies filing stories from Wuhan, Chinese news releases, and firsthand raw video and accounts from people within the city, but the amount of information being released has decreased significantly. We now often find that the earliest accounts of breaking news stories around the world are amateur video captured first hand as an event unfolds. This can be amazingly disturbing and personal when natural disasters or terrorism are involved. They amount to peephole views of larger stories, and can be subject to misinterpretation. We do know that the current mortality rate of infected patients is low, which is a good thing. We also know that the virus can be transmitted before showing any symptoms, which is bad. Some companies have warned that the virus will have an effect on first quarter profits. Travel-related companies have already seen their stocks move appreciably to the downside. We will be watching the trajectory of the spread of the virus closely over the next few weeks.

Earnings results for the fourth quarter have been good enough to allow the markets to stay near their peak and in some cases move higher, even with the uncertainty of the Coronavirus. The largest FAANG stocks have been the leaders, outpacing the market, which leaves little praise for the majority of the stocks in the market. Risk has increased if only because the price increases in the indexes year to date, like last year, have mostly been made up of P/E expansion, not concurrent earnings growth. We continue to emphasize discipline and diversification in our portfolio construction. We hope that a partial resolution of the trade dispute with China, and a revamped North American trade agreement, can provide some tailwind to the economy.

Although the markets have remained strong, we are troubled by the pullback in commodity prices and inflation expectations, and the resumption of a flattening of the yield curve. Some of this is to be expected in light of the uncertainty that surrounds the Coronavirus, but it is troubling nonetheless. The Fed is trying to stay put and keep rates at their current level, but in the last week, the 10 Year Treasury yield dropped below the 3 Month Treasury Bill. An inverted yield curve is never a good sign, and this move is accompanied by lower oil prices and lower inflation expectations. Some clarity on the path of the virus might relieve some of this stress, but the immediate result is that pressure has increased on the Fed for another rate cut. As we have said before, if the market demands action from the Fed, it is usually better to act sooner rather than later. On the positive side, job growth has continued to be robust, housing activity is moving to new highs, and credit spreads are near their all-time tights. All of these things are signs of a healthy economy.

How about the Democratic race for the nomination? Did you think we could ever have bigger surprises than 2008 or 2016? Buckle your seatbelts. We will make no predictions yet, as much could happen over the next few weeks. We have already seen a Buttigieg bump in Iowa, a Biden crash, and a Bernie rise. Maybe there will be more clarity once we get a take on Bloomberg’s impact on the race after Super Tuesday, but as of now, who knows? Bernie Sander’s campaign can be likened to both McGovern in 1972 and Trump in 2016 at this point of the campaign. Politics never ceases to amaze.

Random Thoughts & In Memory of Kobe Bryant: “I have nothing in common with lazy people who blame others for their lack of success. Great things come from hard work and perseverance.”

“The most important thing, the thing that unites all of us, is that we can inspire and challenge one another to be better.” – Kobe Bryant

![]()

Lessons Learned

November 26, 2019

Dow: 28,122

Usually, the lessons that will help us most as investors are the hardest to learn and practice because most useful lessons pertaining to investments are counterintuitive. One is that “group decisions” are many times poor and late. Both individual securities and active investment strategies go through cycles where they outperform and underperform. It is difficult to step up and purchase a security after a period of underperformance, and it is easy to come up with many justifications to purchase a security after a period of outperformance. Buy high and sell low is the rule followed by most inexperienced, emotional investors, trend followers, and pure momentum investors. This is not a way to beat the market. Some degree of contrarianism is essential for significant success. After all, the market itself is a distillation of the groupthink of all the participants in the market. The same biases apply to investment strategy selection. It is easy to hire a manager or strategy after a period of outperformance, but few would recommend hiring a manager or strategy after a period of underperformance. The latter would have to study why the manager or strategy generated the performance it did, and thus involve a deeper understanding than just a cursory review and recommendation based on performance, which can be complicated.

Some believe timing the market is a key to success, but we have not seen any entity succeed at this long term. Even Warren Buffet does not try and time the market. He may have large cash positions, but those are driven by his ability to find discrete investments that meet all of his high hurdles for purchase, not by broad market valuations. Once he establishes a holding, he normally holds it for decades, sometimes through long periods of underperformance. That approach may be extreme, but it has worked for him. We believe in maintaining diversification while being fully invested in all of our investment strategies. We believe the risk profile of every client may differ, and that adjustments should be made outside of the actual strategy. Another lesson we have learned through market cycles is that risk should be added at market lows. This sounds extreme, but it is just the converse of the truism that risk should be reduced at market highs, a notion that few would argue against. Increasing risk in times of stress and uncertainty is also a strategy employed by Buffet, as when he deployed large amounts of capital in 2008 when the market was in turmoil.

If these principles sound contrarian, they are. One way to understand contrarian principles is to think of them as beliefs that sound totally reasonable in the abstract, but are extremely difficult to employ in the heat of the moment. There have been multiple causes of unease recently: in mid-August, the market was disappointed with the quarter point the Fed cut from interest rates at the end of July, earnings in the third quarter were expected to be flat or lower, slower growth and industrial production were expected through the end of the year, the trade deal with China continued to be on again or off again, the specter of impeachment and a trial in the Senate became a real possibility, and the market fell six percent in just the first two weeks of August. None of these concerns have gone away in the last three months, and most have worsened or become more persistent. Nevertheless, the S&P 500 is up over 10% in the last four months – not the outcome many would have predicted. Hedge fund managers, the supposed smart money, have been forced to deploy some of their high cash positions to chase the market, driving the rally to new highs. No, we don’t know how long the rally will continue, but we will ensure that our portfolios will participate by being fully invested, yet diligent in looking for opportunities to improve our holdings.

In bonds, investors have been rewarded for taking more risk and holding longer bonds. That has been true for current holders who have enjoyed price gains as well as income in this bull market for bonds. That will not necessarily be true for investors from this point forward. Credit spreads have remained tight and capital gains for the most part have been preserved, but there is no guarantee this will hold into the future. It looks like yields have hit their low for this year and have begun to head upwards after the last Fed easing. Keep in mind that the Fed wants to see longer rates higher than short rates, even though they don’t often say it publicly. The yield curve is no longer inverted and the Fed can breathe a sigh of relief and spend some time on the economic sidelines instead of in the spotlight. Some contrarians may have missed the rally as they held shorter duration and higher quality securities during this bond bull market, but they are being rewarded most recently.

Please share our best wishes for a happy and restful Thanksgiving holiday with your families.

Random Thought for November 2019: “As we express our gratitude, we must never forget that the highest appreciation is not to utter words, but to live by them.”

John Fitzgerald Kennedy

![]()

Microsoft

October 30, 2019

Dow: 27,817

Even as Microsoft and Apple vie for the title of the largest company by market capitalization in the S&P 500 Index, Microsoft has garnered little attention over the last few years. It did not even merit a letter in the FAANG (Facebook, Apple, Amazon, Netflix, Google) acronym. But Microsoft is arguably the one company that has brought about the greatest changes in society in the past fifty years. Its founder, Bill Gates, is possibly the most important entrepreneur since Henry Ford. Most businesses communicate using Outlook and Word, compile and analyze data using Excel, and develop and present ideas and goals using PowerPoint. Bill Gates’ story would seem to confirm that entrepreneurs are born, not made. He has an insatiable hunger for knowledge and advancement, and has set as a goal for his remaining years, the wholesale improvement of the human condition.

Bill Gates celebrated his 64th birthday this week. He founded Microsoft in Albuquerque, not Seattle, when he was 19. He created his first company, called Traf-o-Data, when he was in high school. The goal of that company was to process collected traffic data at a lower cost than competitors. The company did not succeed; yet real entrepreneurs do not accept failure, but move on to the next project. Microsoft became a success in the late 1970’s and was challenged by Apple in the 1980’s, as Apple developed the GUI, or graphical user interface. Undeterred, Microsoft developed Windows in the 1980’s and was able to drive Apple close to bankruptcy in the 1990’s. Fortunately, they made a deal in 1997 that helped save Apple and has allowed consumers to enjoy their numerous developments.

The Dana Large Cap Equity Strategy was a holder of Microsoft when the Strategy was initially implemented in 1999. The Strategy has bought and sold the Company three times since then, and has held the Company in the Strategy since 2015. Since mid-2015, Microsoft has more than tripled its stock price, with annualized gains of over 30%, placing it in the top five percent of the S&P 500 Index in performance over that period. The Company is currently held in all of the large cap Dana strategies.

What have we learned as a result of following and owning Microsoft over a period of twenty years? Success is a combination of leadership and execution. The leadership of the Company must see where resources should be deployed to succeed in the future, and then must execute on its plan to take advantage of market opportunities. One does not work without the other. Even successful companies will have missteps, and their stock price will go sideways or down for an extended period of time. Microsoft missteps include buying an online advertising company in 2007 for $6 billion dollars and Nokia’s phone business for $7 billion, both ultimately written off. As their business lines continued to evolve, Microsoft laid off approximately 20% of its employee base between 2014 and 2016. In our dynamic economy, even successful companies must evolve or wither.

Over the last three years, Microsoft has focused significantly on business services and cloud computing. Providing services to businesses has been a faster growing segment and has helped supplant the slow-growing, low-margin legacy businesses at Microsoft. Microsoft has grown to be the second largest supplier of cloud computing services behind Amazon, and that business is projected to grow revenues to six times their current level over the next five years. Cloud computing services are one of the most highly profitable businesses as well, with gross profit margins of 40-70%. Microsoft was just announced as the winner of a U.S. Department of Defense contract that could provide $10 billion of revenue over the next ten years. Amazon was previously thought to be the front runner for the business.

If anyone has an interest in how Bill Gates has pivoted personally from Microsoft to philanthropy, we recommend the Netflix documentary Inside Bill’s Brain. He is as persistent in tackling world problems as he was in leading Microsoft.

Random Thought for October 2019: “I really had a lot of dreams when I was a kid, and I think a great deal of that grew out of the fact that I had a chance to read a lot.”

Bill Gates

![]()

Dollars and Sense

September 30, 2019

Dow: 26,917

We need more of both. The U.S. and global economies need more dollars in circulation, and our political leaders need better judgement (sense). Did President Trump cross the “high crimes and misdemeanors” line in his call with the Ukrainian President? Will it make political sense for the Democrats to push forward with an impeachment inquiry and vote? The political stakes have ratcheted higher for both parties with more than a year to go until the general election. We don’t have a call yet on who it will benefit and who it will hurt, although Joe Biden had already been falling in the polls and the prediction markets relative to Elizabeth Warren. If there is slippage in the economy prior to the election, she has positioned herself to be the beneficiary. Polls released recently are as expected; about 4 in 10 think the President should be impeached, 4 in 10 do not, and 2 in 10 say it is too soon to tell. The battle is for those ”swing thinkers.” Some say they are not thinkers at all, since their opinions can vacillate, but that is where both parties think they have an advantage. The Democrats think the issue and the timing are right to ramp up talk of impeachment. The President believes that ultimately he will be vindicated and this will again be seen as a witch hunt. Get ready for more outrage overload from both sides. It appears the markets may have become dulled by the constant political outrage, as they have not moved much on the new political developments.

What has changed in the market over the last few weeks is the leadership. The areas of the market that had been outperforming, including technology and high valuation stocks, some with no earnings, have begun to falter. Stocks that had been underperformers, including many value and dividend stocks, have begun to outperform. If we use the Russell 1000 Value and Growth indexes as proxies for these stock categories, the growth index has generated double the return of the value index over the last five years. For the first eight months of this year, the growth index led the value index by more than 9%. In September, that gap has been cut in half, to less than 4.5%. Why is this important? A healthy market does change leadership periodically, or at least shows a reversal of trends when one class of companies or market sector significantly outperforms another. To use a sports team analogy, many winning teams have a few superstars, but those teams cannot win consistently if many other players are far below average. When one class of companies significantly outperforms the other, eventually that gap has to close. If it closes by the leaders falling significantly, you have a falling market. If it closes by the old leaders pausing and the laggards beginning to outperform, there may be more market gains to come. Economic indicators have also begun to surprise on the upside, indicating that many participants have become too pessimistic about the economy and the markets. We root for a healthy market where there is not a huge divergence between the haves and the have nots.

We have saved what may be the least interesting topic for last, which is the recent tumult in the repo markets. The repo market provides a place where banks and brokerage houses can borrow and lend to each other on a short-term basis, collateralized by securities, usually U.S. Treasuries. When strange things happen in this market, it is frequently referred to as a problem with the “plumbing” in the market. The repo market allows institutions with securities to use them as collateral to borrow cash, so plumbing is actually an appropriate metaphor. Late in September the rate on repo loans began to rise significantly, indicating a shortage of dollars to loan. While weak treasury auction demand, declining treasury prices and high quarterly tax payments received the blame, the New York Fed did not address the problem immediately by adding dollars to the market. Was this a more ominous sign of things to come? We don’t think so. The New York Fed could have been less clumsy in addressing the need for dollars, and they have said they will address the need better in the future. We will watch the issue going forward.

Good news still exists: the S&P 500 closed within half of a percent of its previous all-time high in September, the Fed thought it prudent to provide another rate cut, and many broad economic indicators are stable to rising. We will continue to mind the dollars entrusted to us and be on the lookout for adjustments that need to be made to our strategies.

Random Thought for September 2019: “Which future do you want? Do you want the future where we become a space-ranked civilization and are in many worlds and out there among the stars? Or one where we are forever confined to Earth? And I say it is the first.” – Elon Musk – Starship Rocket Unveiling 9/28/19

![]()

Keep on Truckin’

July 31, 2019

Dow: 26,864

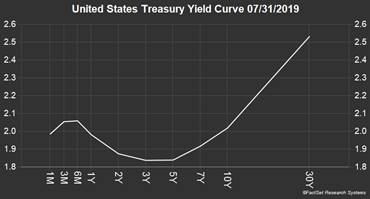

The current U.S. economic expansion has now passed the ten-year mark, and has set the record for the longest expansion on record. During that period, we have had three quarters of negative GDP growth, but in every case the economy bounced back the following quarter. The discussion has now moved to how to keep this expansion going. We can review the headwinds and tailwinds that currently coexist in the economy, but ultimately, we have to focus on the elephant in the room that underlies the Federal Reserve’s concern – the inverted yield curve.

First let’s look at what is working. The unemployment rate has been at 4% or below since last spring, and even with some signs of economic slowing, there is no indication that the rate will rise materially in the near future. Other labor market indicators that could indicate an overheating labor market would include weekly hours worked and capacity utilization and neither has moved up significantly in recent months. Some point to average hourly earnings growth moving above 3%, but this just moves wage growth back to the long-term average after a decade of subpar growth. New and existing home sales have remained strong, and growth in home prices has slowed somewhat, which may bode well for a continued strengthening of the housing market. Reasonable home price growth prevents prices from significantly outpacing income growth. The stock market has provided the big positive surprise this year, although you wouldn’t know it from reading the economic headlines. The S&P 500 is now up over 20% in the first seven months of the year. The bond market has participated as well, with Treasuries, agencies, and corporates all showing strong total returns this year.

There are reasons to worry, and China and tariffs are one concern. The tariffs have not seemed to make a significant dent in overall economic growth, although they have led to disruption in some industries and caused significant supply chain modifications. Overall global growth has been voiced as a concern by the Fed, and they seem to be more concerned that slow overseas growth could be more of a drag on our economy than it has been in the past. Market valuations in the U.S. are a concern, as earnings growth has slowed and the price to earnings ratio of the S&P 500 has moved back up to near 18 times. It is also troubling that small cap stocks have not fully participated in the move to new market highs, as the Russell 2000 index is still down almost 8% from its high last summer.

It seems to us that the elephant in the room is the yield curve. A negatively sloped yield curve can be telling us many things about the economy and the markets. It can tell us there is an aversion to risk taking. It can be telling us that there are too few investment opportunities that can be perceived as fairly priced. It can be telling us that market participants are concerned that economic conditions will weaken soon. The Fed can address a flat or negative yield curve by cutting rates, and time is of the essence. The irony for the Fed is that if they move more aggressively to lower rates, they may not have to cut as much as they will if they drag their feet. The three-month Treasury bill has had a yield above the ten-year Treasury for about nine weeks. If the economy is a car, the analogy would be a low fuel light that comes on. Can you keep driving for a while? Sure, but the risk increases the further you go. Post yesterday’s Fed decision, yields on the short end of the curve rose and rates on the long end of the curve fell. The stock market fell. Chairman Powell, it is long past time to listen to the markets.

Random Thought for July 2019: “Internet can destroy our party and our country” – Xi Jinping, President of the People’s Republic of China